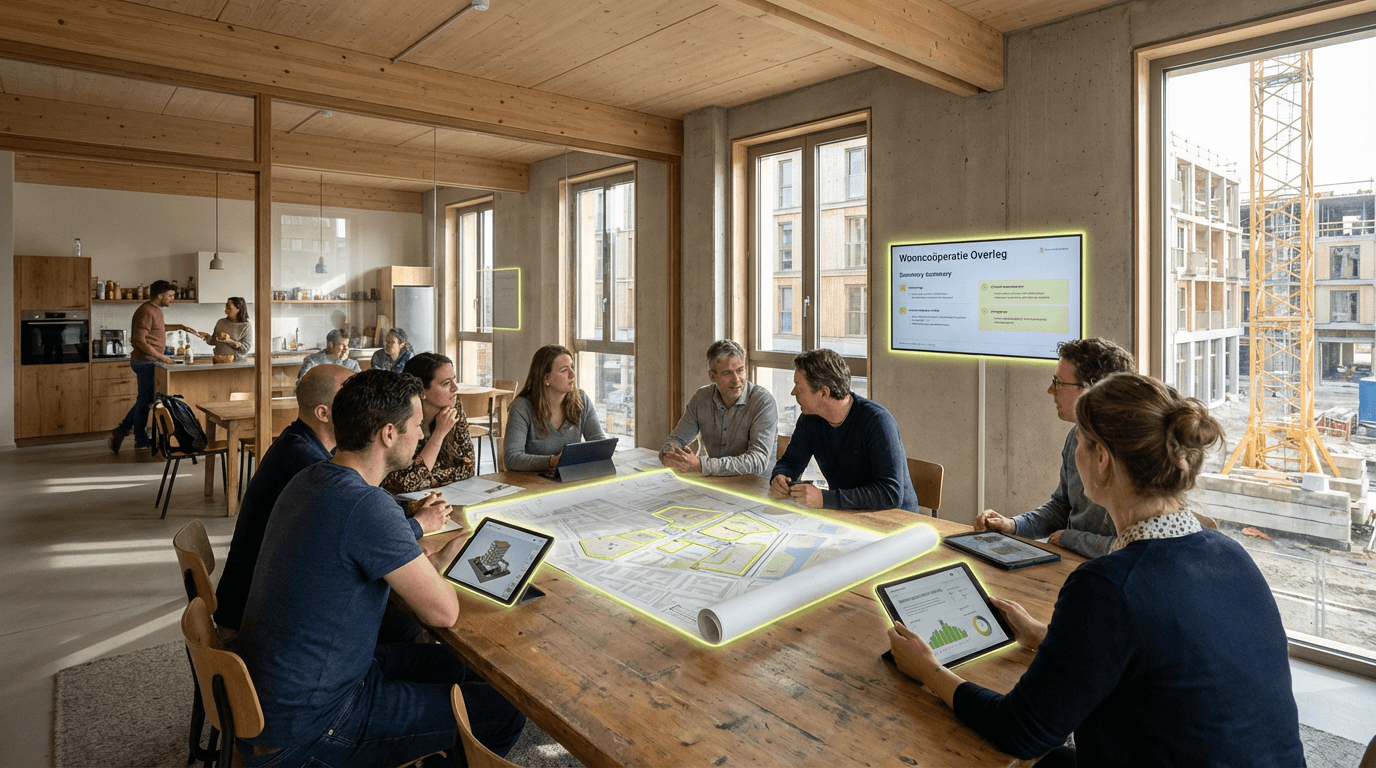

Wooncooperaties (Housing Cooperatives)

Housing cooperatives represent a fundamental shift in how communities approach residential ownership and governance, moving away from purely market-driven or state-provided housing toward collective ownership models where residents hold both equity stakes and decision-making power. This organizational form addresses several persistent challenges in the Benelux housing landscape: affordability pressures in tight urban markets, the need for long-term stewardship that balances maintenance with community stability, and the desire for resident agency in an increasingly financialized housing sector. In the Netherlands, housing cooperatives have deep historical roots, with some associations managing thousands of units and playing significant roles in neighborhood development. Belgium has seen renewed interest in cooperative models, particularly among younger residents seeking alternatives to conventional homeownership or rental markets, while Luxembourg's smaller cooperative initiatives reflect early experimentation with community-led housing in a high-cost environment. The cooperative structure matters because it decouples housing from speculative investment cycles, creating stability for residents while potentially offering a governance framework that can integrate sustainability goals, social mixing, and participatory planning more effectively than traditional development models.

The mechanics of housing cooperatives vary across contexts, but generally involve members purchasing shares that grant both residence rights and voting power in collective decisions about property management, renovation priorities, tenant selection, and long-term strategic direction. Financing remains a critical challenge: cooperatives typically require patient capital willing to accept lower returns than conventional real estate investment, often sourced through ethical banks, municipal loan guarantees, or member contributions pooled over time. In the Netherlands, established housing associations benefit from historical capital accumulation and regulatory frameworks that recognize their quasi-public role, while newer Belgian cooperatives often operate at smaller scales, sometimes combining co-housing principles with cooperative ownership structures. Democratic governance introduces complexity—decision-making processes must balance efficiency with inclusivity, and cooperatives report ongoing tensions around maintenance standards, financial contributions, and the pace of sustainability upgrades. Early evidence suggests that successful cooperatives invest heavily in governance capacity-building, establishing clear decision frameworks and conflict resolution mechanisms before operational challenges emerge. The model's scalability remains uncertain: while individual cooperatives demonstrate viability, replicating the approach across housing markets requires supportive regulatory environments, accessible financing mechanisms, and sufficient organizational capacity among resident groups.

For policymakers and housing strategists, cooperatives signal potential pathways toward more resilient, community-anchored housing systems, particularly in contexts where neither pure market provision nor traditional social housing adequately serves middle-income residents or addresses sustainability transitions. Monitoring should focus on whether cooperative models can move beyond niche applications to influence broader housing supply, particularly as municipalities experiment with land allocation policies that favor cooperative bids or as financial institutions develop dedicated cooperative lending products. Critical thresholds include the emergence of secondary support infrastructure—cooperative development consultancies, shared legal frameworks, inter-cooperative financing mechanisms—that would reduce barriers to formation and operation. The approach also raises questions about long-term governance sustainability: as founding members age or move, can cooperatives maintain participatory cultures and financial discipline? Observers should track whether cooperatives successfully integrate diverse income groups or inadvertently become exclusive communities, and whether their governance structures prove adaptable to climate adaptation requirements and changing neighborhood demographics. The cooperative signal matters less as a universal housing solution than as an indicator of growing demand for ownership models that prioritize use value and community stability over exchange value and individual wealth accumulation.