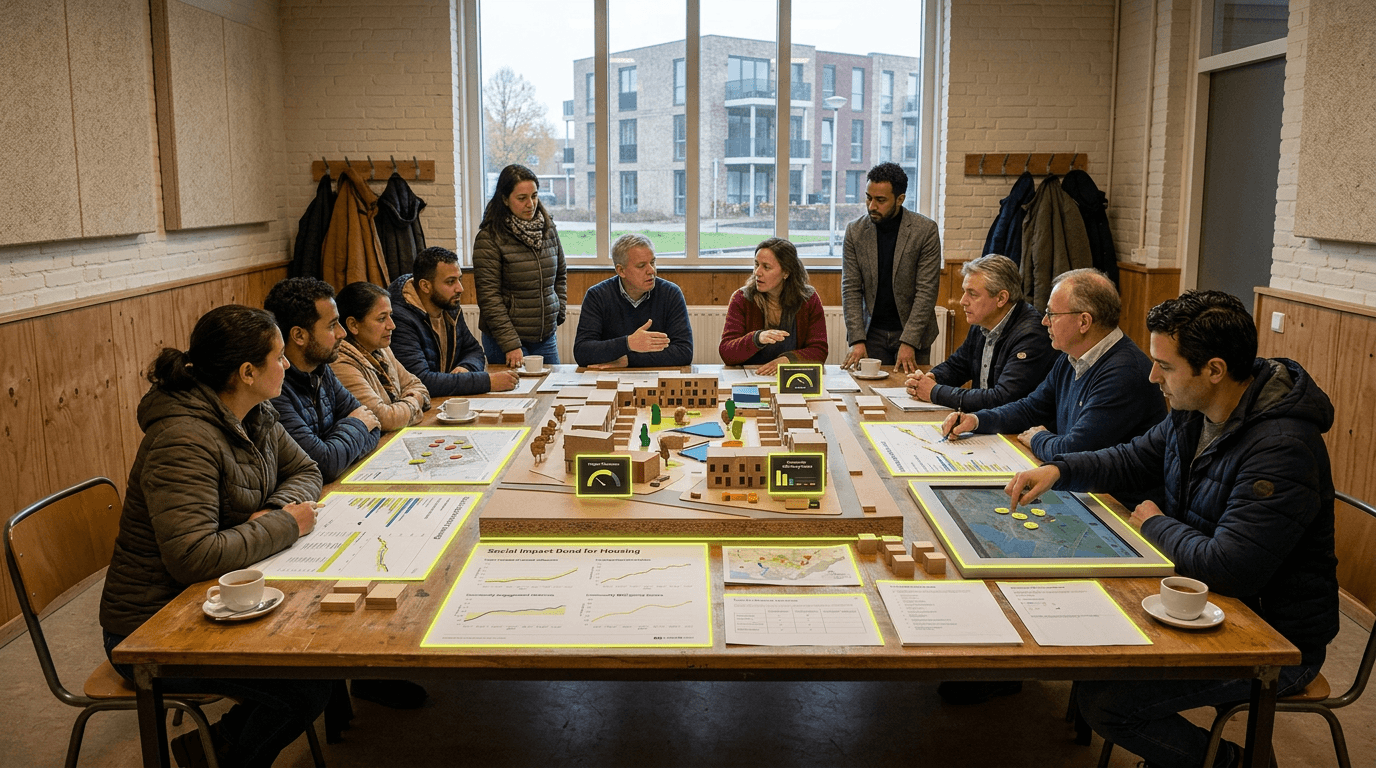

Social Impact Bonds for Housing

Social Impact Bonds for housing represent a fundamental shift in how public authorities finance social interventions, addressing a persistent challenge in housing policy: the gap between urgent social needs and constrained public budgets. Traditional government funding models often struggle to scale preventive housing interventions or innovative support programs due to budget cycles, risk aversion, and difficulty demonstrating value before implementation. SIBs attempt to solve this by transferring financial risk to private investors who provide upfront capital for housing programs—ranging from homelessness prevention to energy efficiency retrofits—with returns paid by government only when predetermined social outcomes are achieved. This outcome-based financing model creates incentives for service providers to focus on measurable impact rather than simply delivering activities, while enabling public authorities to pay for results rather than inputs. The mechanism matters because it potentially unlocks new capital sources for housing challenges that generate long-term public savings but require patient, risk-tolerant investment.

Early implementations across the Benelux region and broader European context reveal both the promise and complexity of this approach. Pilot programs have targeted homelessness reduction, where investors fund intensive case management and supportive housing services, with government repayment triggered by metrics such as sustained housing tenure, reduced emergency service usage, or improved employment outcomes. Energy retrofit SIBs have emerged where private capital finances insulation and heating system upgrades in social housing, with returns linked to verified energy savings and tenant health improvements. Research from these early deployments indicates that successful SIBs require extensive upfront work to define robust outcome metrics, establish credible measurement systems, and negotiate complex multi-party contracts involving investors, service providers, government agencies, and often independent evaluators. Transaction costs can be substantial—sometimes representing significant portions of total program budgets—raising questions about efficiency at smaller scales. There is also emerging evidence that outcome selection can inadvertently narrow program focus toward easily measurable results while neglecting harder-to-quantify but equally important social benefits.

The implications for housing policy extend beyond immediate financing. If SIBs demonstrate that private capital can profitably address social housing challenges, they may catalyze broader shifts toward outcome-based commissioning and performance management in public housing systems. However, critical questions remain about whether this model genuinely transfers risk or simply creates expensive intermediation, whether outcome metrics adequately capture social value or create perverse incentives, and whether the approach works better for certain interventions than others. Monitoring should focus on comparative cost-effectiveness against traditional procurement, the quality and sustainability of outcomes achieved, and whether SIBs genuinely enable innovation or primarily repackage existing interventions. The scalability threshold appears contingent on reducing transaction costs through standardization while maintaining the flexibility needed for context-specific housing challenges—a tension that will likely define whether this remains a niche financing tool or becomes mainstream infrastructure for social housing investment.