Electric Vehicle Assembly & Integration

Geography: Americas · South America · Latin America

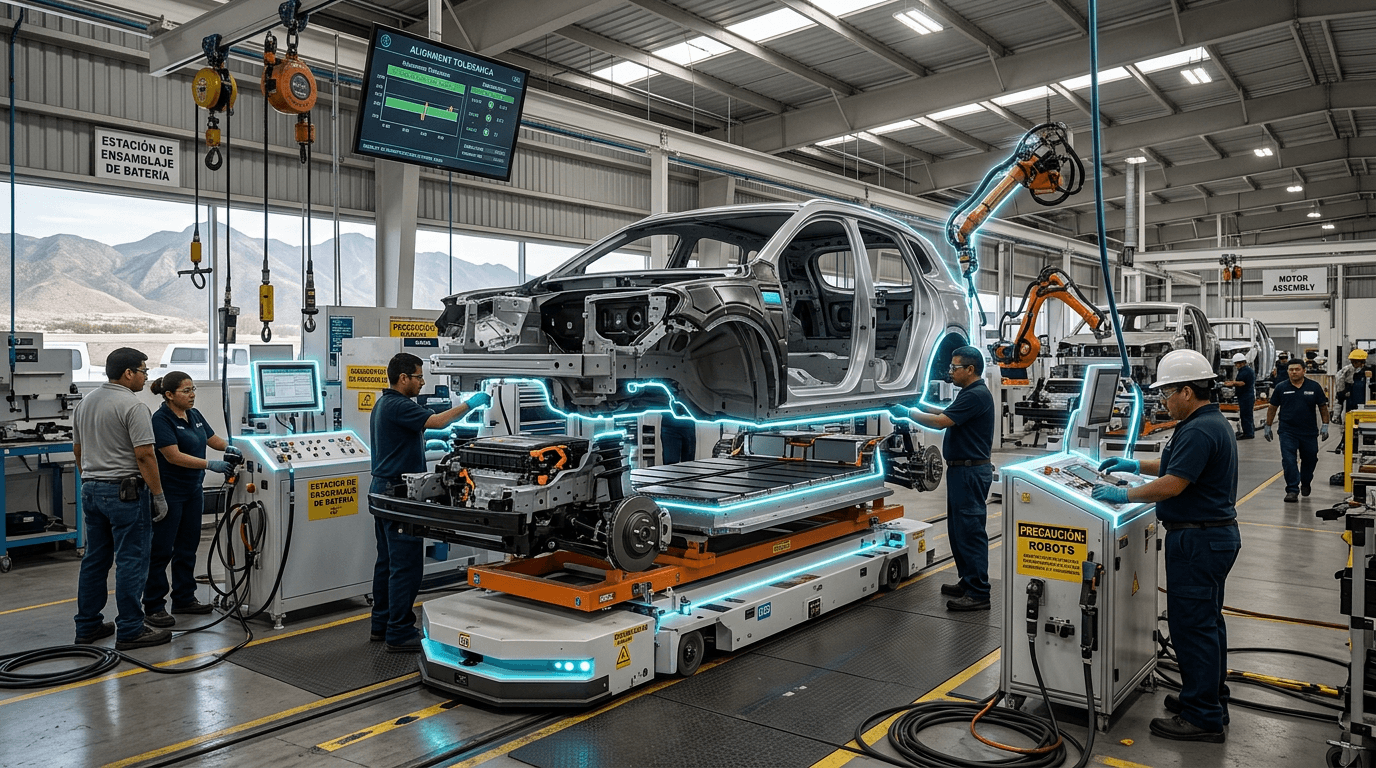

Mexico is emerging as a major electric vehicle manufacturing hub, with EV production up 72% in early 2025 compared to the same period in 2024. The country's existing automotive infrastructure — already the world's 7th-largest vehicle producer — is being retooled for electrification. Tesla announced a $5 billion gigafactory near Monterrey (currently delayed by tariff uncertainty), while BMW, Volkswagen, and Chinese manufacturers are expanding EV-specific assembly lines in existing Mexican plants.

The technology focus is on integrated EV assembly platforms: battery pack integration, electric drivetrain installation, thermal management systems, and software-defined vehicle architecture. Mexico's advantage is not just labor cost but the existing supplier ecosystem — thousands of Tier 1 and Tier 2 automotive suppliers already operate in the country, and many are pivoting to EV-specific components including wiring harnesses for high-voltage systems, lightweight structural components, and power electronics.

The geopolitical dimension is critical. USMCA rules of origin require 75% North American content for tariff-free trade — EVs assembled in Mexico with North American components can enter the US duty-free, while those with excessive Chinese content cannot. This creates a powerful incentive structure that pulls EV manufacturing to Mexico, even as US tariff policy creates short-term uncertainty. The question is whether Mexico can move beyond assembly into higher-value battery cell manufacturing and powertrain R&D.