Semiconductor Test and Metrology Equipment

Geography: Asia Pacific · East Asia · Japan

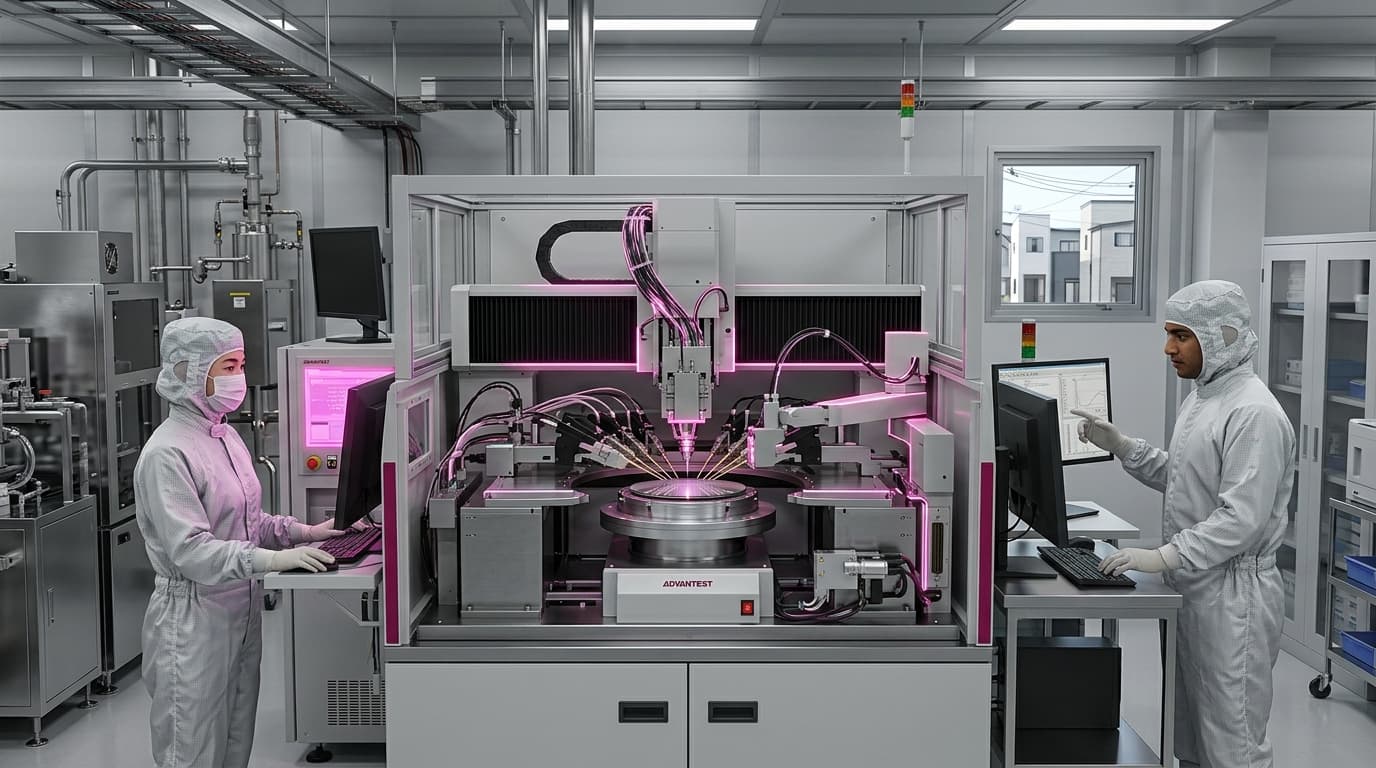

Advantest controls approximately 55% of the global semiconductor automated test equipment (ATE) market, testing every advanced chip before it ships. Disco Corporation dominates wafer dicing and grinding equipment, and Lasertec holds a monopoly on EUV photomask inspection systems — the only company in the world capable of inspecting the masks used in EUV lithography. These niche monopolies are individually smaller than TEL but collectively essential.

Advantage's position is amplified by the AI chip boom — every NVIDIA H100/B200, every AMD MI300, every custom AI accelerator must pass through Advantest equipment for testing. AI chips are larger and more complex than previous generations, requiring more test time per chip and driving Advantest's revenue growth. Lasertec's EUV mask inspection monopoly is perhaps the semiconductor industry's most extreme single-company dependency after ASML.

Japan's collection of semiconductor equipment niche monopolies — coating, testing, inspection, dicing — creates systemic leverage that exceeds what any single company provides. The equipment ecosystem in Japan is interdependent: advances in one area (e.g., new photoresist chemistry) require corresponding advances in equipment (new coater designs, new metrology tools), creating a self-reinforcing innovation cluster centered in the Tokyo-Osaka industrial corridor.