Spodumene-to-Lithium-Hydroxide Refining

Geography: Asia Pacific · Oceania · Australia New Zealand

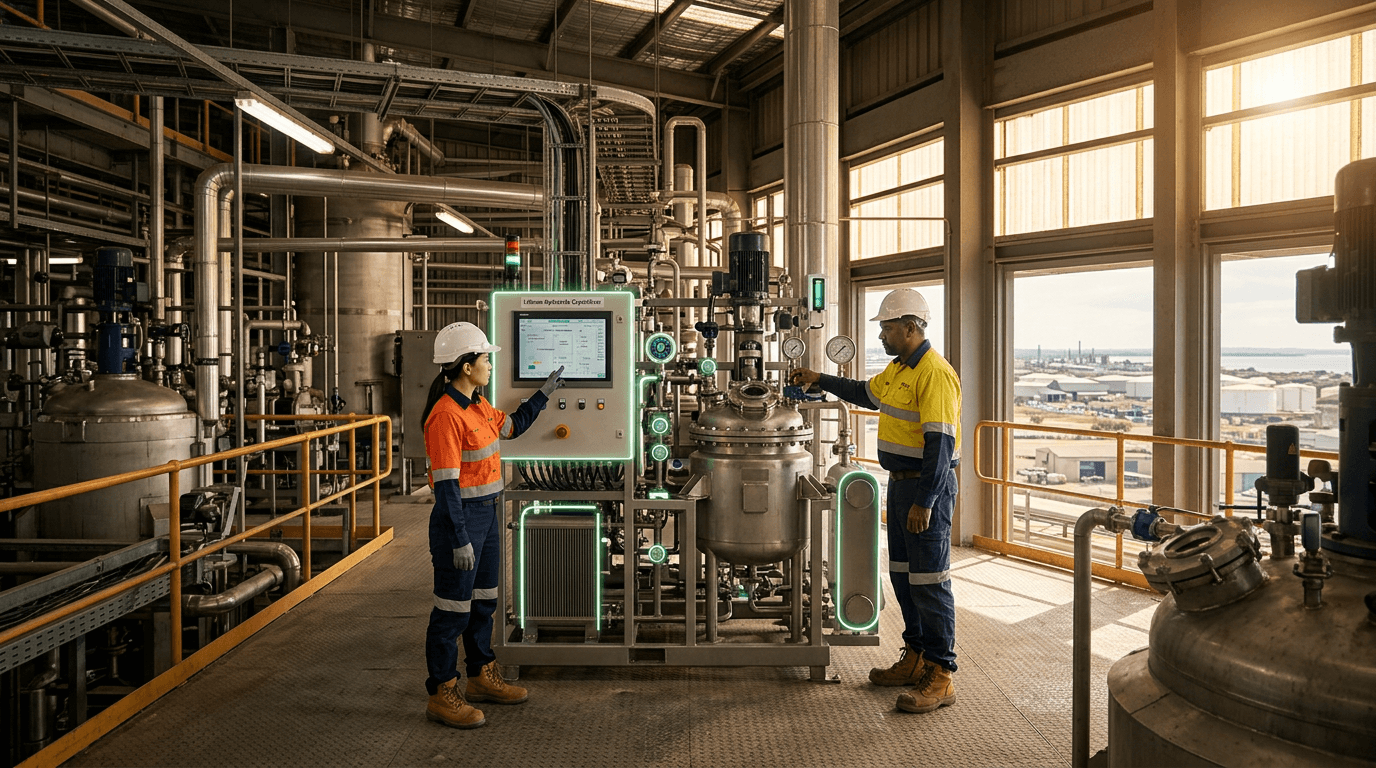

Australia is the world's largest lithium producer from hard-rock (spodumene) mining but has struggled to master downstream refining into battery-grade lithium hydroxide. The Tianqi-IGO joint venture's Kwinana refinery — designed for 24,000 tonnes per annum — faced persistent commissioning challenges and underperformance, with Tianqi terminating Phase 2 construction in January 2025 and IGO reporting low confidence in the asset by August 2025. Albemarle also exited its Australian lithium hydroxide plans, creating both a setback and an opportunity for local players.

Converting spodumene concentrate to battery-grade lithium hydroxide (LiOH·H₂O, ≥56.5% purity) involves complex multi-stage chemical processing: calcination at 1,050°C, acid roasting, leaching, impurity removal, and crystallization — each requiring precise control. The technology has been dominated by Chinese processors who refined it over decades with government support. Australia's attempts to replicate this domestically encountered a steeper learning curve than anticipated, with the Kwinana experience demonstrating that first-of-kind processing facilities need extended ramp-up periods.

Despite setbacks, the strategic imperative remains. Australia exports ~300,000 tonnes of spodumene concentrate annually, capturing perhaps $2,000/tonne, while battery-grade lithium hydroxide sells for $15,000-25,000/tonne. Mastering downstream processing would multiply the value captured domestically by 5-10x. The lessons from Kwinana's challenges are informing next-generation refinery designs with improved process control and lower capital costs, while the Critical Minerals Strategy provides policy support for continued investment in domestic refining capability.

Research this in Signals

Signals turns a topic into a sourced research record you can inspect and rerun. Your first scan is free, and this one starts with Spodumene-to-Lithium-Hydroxide Refining already loaded, so edit it or scan as is.