Industrial Robotics in Automotive Manufacturing

Geography: Americas · South America · Latin America

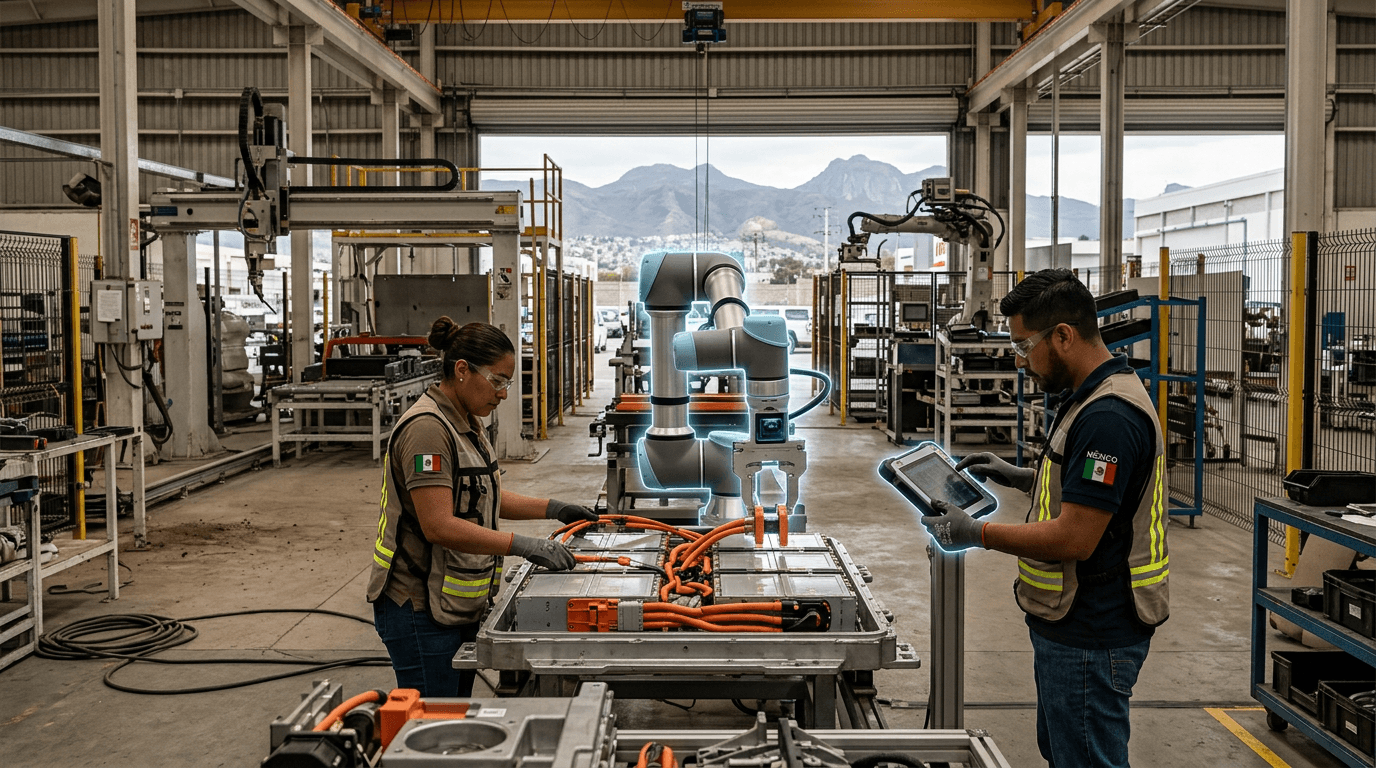

Mexico's automotive manufacturing sector operates one of the densest concentrations of industrial robots in Latin America — over 30,000 units performing welding, painting, material handling, and assembly across plants in Nuevo León, Guanajuato, Puebla, and Aguascalientes. The transition to EV manufacturing is accelerating robotics adoption, particularly collaborative robots (cobots) for battery module assembly, adhesive application, and quality inspection tasks that require precision beyond human capability.

The technology evolution includes vision-guided robotics for flexible assembly (handling multiple vehicle variants on the same line), AI-powered quality inspection using machine vision to detect defects at line speed, and digital twin integration that simulates production changes before physical implementation. Mexican plants operated by BMW, Volkswagen, and Toyota increasingly mirror the automation levels of their German and Japanese counterparts.

The strategic tension is between automation and Mexico's labor cost advantage. If robots can do the work, why not locate the factory closer to the end market? The answer lies in total cost optimization: even highly automated plants need skilled technicians, and Mexico offers competitive engineering salaries. More importantly, the existing supplier ecosystem and logistics infrastructure make Mexico's total landed cost lower than reshoring to the US, even with automation parity.