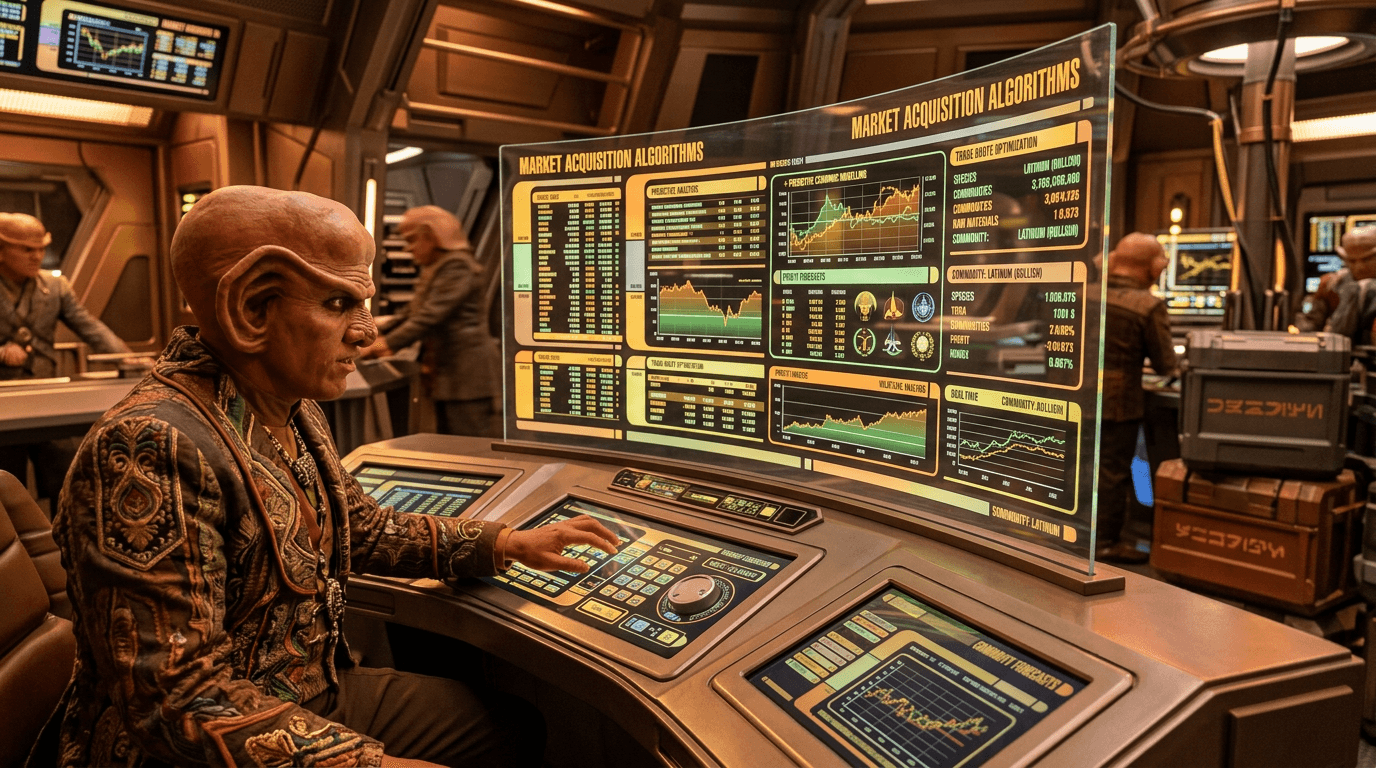

Acquisition Computers / Profit Algorithms

Acquisition computers represent a speculative class of advanced computational systems designed to optimize economic transactions through predictive modeling and strategic analysis. These systems are imagined to operate at the intersection of artificial intelligence, behavioral economics, and game theory, processing vast arrays of market data, historical transaction patterns, and psychological profiles to identify optimal negotiation positions and trading strategies. The concept extends beyond simple algorithmic trading to encompass comprehensive decision-support systems that could theoretically model complex multi-party negotiations, predict competitor responses, and dynamically adjust strategies in real-time. While contemporary algorithmic trading systems and business intelligence platforms share some conceptual DNA with this vision, the fully realized acquisition computer remains largely in the realm of science fiction, representing an idealized fusion of perfect information processing and strategic omniscience that current technology cannot achieve.

The narrative appeal of acquisition computers lies in their representation of economic power concentrated through technological superiority. In speculative scenarios and corporate strategy discussions, these systems embody the ultimate competitive advantage—the ability to consistently outmaneuver rivals through superior predictive capabilities and strategic optimization. This concept resonates with contemporary anxieties about algorithmic dominance in financial markets and the increasing role of machine learning in business decision-making. The profit algorithm component suggests a future where human intuition and experience in negotiation become subordinate to computational analysis, raising questions about the nature of value creation, the ethics of information asymmetry, and the potential for technological systems to exploit cognitive biases at scale. Such systems appear in strategic planning exercises as both aspirational tools and cautionary examples of over-reliance on quantitative optimization.

The plausibility of acquisition computers depends heavily on several unresolved challenges in artificial intelligence and economic modeling. While machine learning systems excel at pattern recognition within constrained domains, the chaotic nature of real-world markets, the unpredictability of human behavior, and the fundamental uncertainty inherent in complex economic systems present significant barriers to the kind of comprehensive predictive capability these systems would require. Current algorithmic trading demonstrates both the potential and limitations of computational approaches—capable of executing strategies at superhuman speeds but vulnerable to unexpected market conditions and prone to amplifying systemic risks. The development of more sophisticated acquisition systems would require breakthroughs in causal reasoning, robust uncertainty quantification, and the ability to model emergent phenomena in complex adaptive systems. Even with such advances, the adversarial nature of markets suggests that widespread deployment of similar systems would quickly erode any predictive advantage through competitive adaptation, potentially leading to an arms race of increasingly sophisticated but mutually negating algorithms.