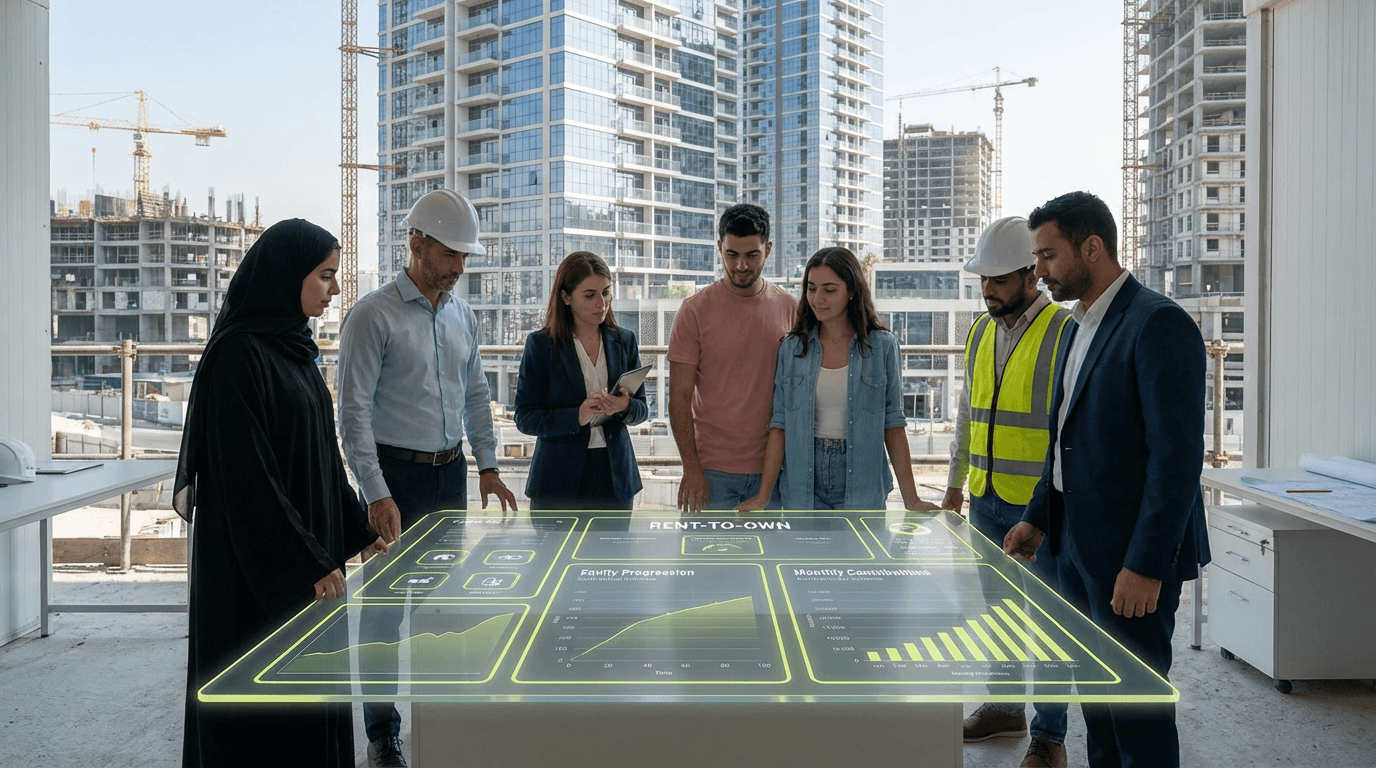

Rent-to-Own (RTO) Schemes

Rent-to-Own schemes represent a contractual innovation designed to address a fundamental mismatch in Gulf housing markets: a growing mid-income workforce that can sustain monthly housing costs but cannot access the capital reserves required for conventional mortgage down payments. In markets where central banks typically mandate 20-25% down payments and where expatriate populations face additional financing barriers due to residency status, RTO arrangements create an alternative pathway by converting rental payments into gradual equity accumulation or securing future purchase options at predetermined prices. This matters because it directly confronts the region's dual challenge of maintaining economic competitiveness through talent retention while managing the social implications of a largely transient, non-asset-holding workforce. As Gulf economies diversify beyond oil dependence and seek to attract knowledge workers for longer tenures, the inability of mid-tier professionals to build wealth through housing becomes both an economic and demographic vulnerability.

The mechanics of RTO schemes vary, but most operate through hybrid contracts where a portion of monthly rent—often 20-40%—is credited toward a future purchase, or where tenants secure a fixed-price purchase option exercisable after two to five years of occupancy. Early deployments in UAE and Saudi Arabia suggest multiple drivers converging: developers seeking to clear inventory in cooling markets without steep discounts, governments pursuing homeownership targets as part of national vision frameworks, and employers exploring housing benefits that enhance retention without direct salary increases. Industry observers note that RTO uptake remains concentrated in mid-market developments rather than premium segments, and that contract enforcement mechanisms are still evolving across GCC jurisdictions. The model faces uncertainty around what happens when tenants exit early, how equity portions are calculated during market downturns, and whether regulatory frameworks will standardize terms to prevent predatory structures.

The implications extend beyond individual transactions to reshape workforce dynamics and urban development patterns. If RTO schemes scale successfully, they could stabilize expatriate populations in ways that traditional rental markets cannot, potentially shifting demand toward suburban family-oriented developments rather than transient urban cores. Policymakers should monitor whether these arrangements genuinely build household wealth or simply extend debt obligations under different terms, particularly if property values stagnate. Key thresholds to watch include the percentage of new developments incorporating RTO options, default rates compared to conventional mortgages, and whether secondary markets emerge for trading RTO contracts. The signal also raises questions about how cities plan infrastructure when residential populations become less fluid, and whether RTO models might eventually extend to commercial real estate as regional economies seek to anchor small businesses and entrepreneurs through similar equity-building mechanisms.

Related Organizations

A major property developer in the UAE known for affordable luxury.

Abu Dhabi's leading developer, with a significant recurring income portfolio from investment properties (residential and commercial).

The regulatory arm (RERA) operates the 'Mollak' system, a mandatory digital platform for payment of service charges and management of Owners Associations.

Azizi Developments

United Arab Emirates · Company

A leading private developer in Dubai.

UAE-based proptech streamlining the home buying process with digital mortgage brokerage and closing services.

A private developer focused on integrated lifestyle communities like Town Square Dubai.

One of the largest real estate management and development companies in Dubai, managing a vast portfolio of rental assets.

An Islamic commercial bank based in the Emirate of Ajman.