Chile Green Hydrogen Export Hub (Magallanes)

Geography: Americas · South America · Latin America

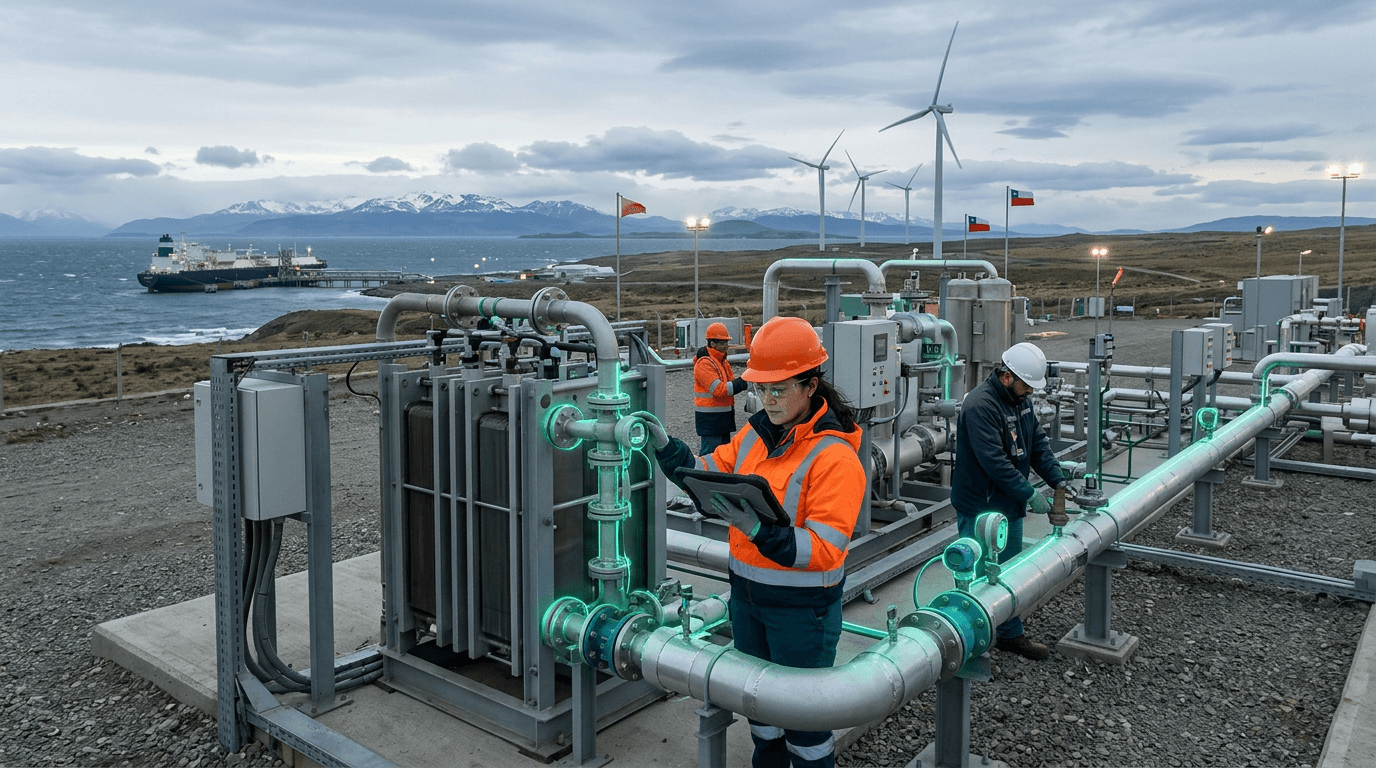

Chile's Magallanes region at the southern tip of Patagonia possesses what may be the planet's most favorable conditions for green hydrogen production: sustained wind speeds averaging 10–12 m/s that yield capacity factors above 60% — nearly double the global average for wind farms. Multiple mega-projects are converging here, most notably HyEx (a joint venture between Engie and Enaex) planning an 18,000-tonne ammonia pilot by 2025–2026 before scaling to 700,000+ tonnes annually, and TotalEnergies' H2 Magallanes project valued at over $16 billion targeting massive hydrogen-to-ammonia production for export.

Chile's green hydrogen ambitions address a structural opportunity: the country has world-class renewable resources but a small domestic market. Converting cheap wind and solar electricity into hydrogen and ammonia creates an exportable energy commodity — essentially bottling Patagonian wind for shipment to industrial markets in Japan, South Korea, Germany, and the Netherlands. Chile's national hydrogen strategy, launched in 2020, aims for 5 GW of electrolyzer capacity by 2025 and 25 GW by 2030, with the goal of producing the world's cheapest green hydrogen at under $1.50/kg.

The strategic implications are substantial. If Chile executes even a fraction of its pipeline, it becomes a first-mover in the global green hydrogen export market — a position analogous to Qatar's role in LNG. The Magallanes projects also represent a potential economic lifeline for a region historically dependent on oil extraction and sheep farming. Key risks include electrolyzer supply chain bottlenecks, port infrastructure gaps, and whether the cost of shipping hydrogen-derived ammonia across the Pacific can compete with locally produced alternatives in Asia. Chile's sharp ramp-up projected for 2030–2032 will be the critical test.

Research this in Signals

Signals turns a topic into a sourced research record you can inspect and rerun. Your first scan is free, and this one starts with Chile Green Hydrogen Export Hub (Magallanes) already loaded, so edit it or scan as is.