Export-Scale Green Hydrogen Production

Geography: Asia Pacific · Oceania · Australia New Zealand

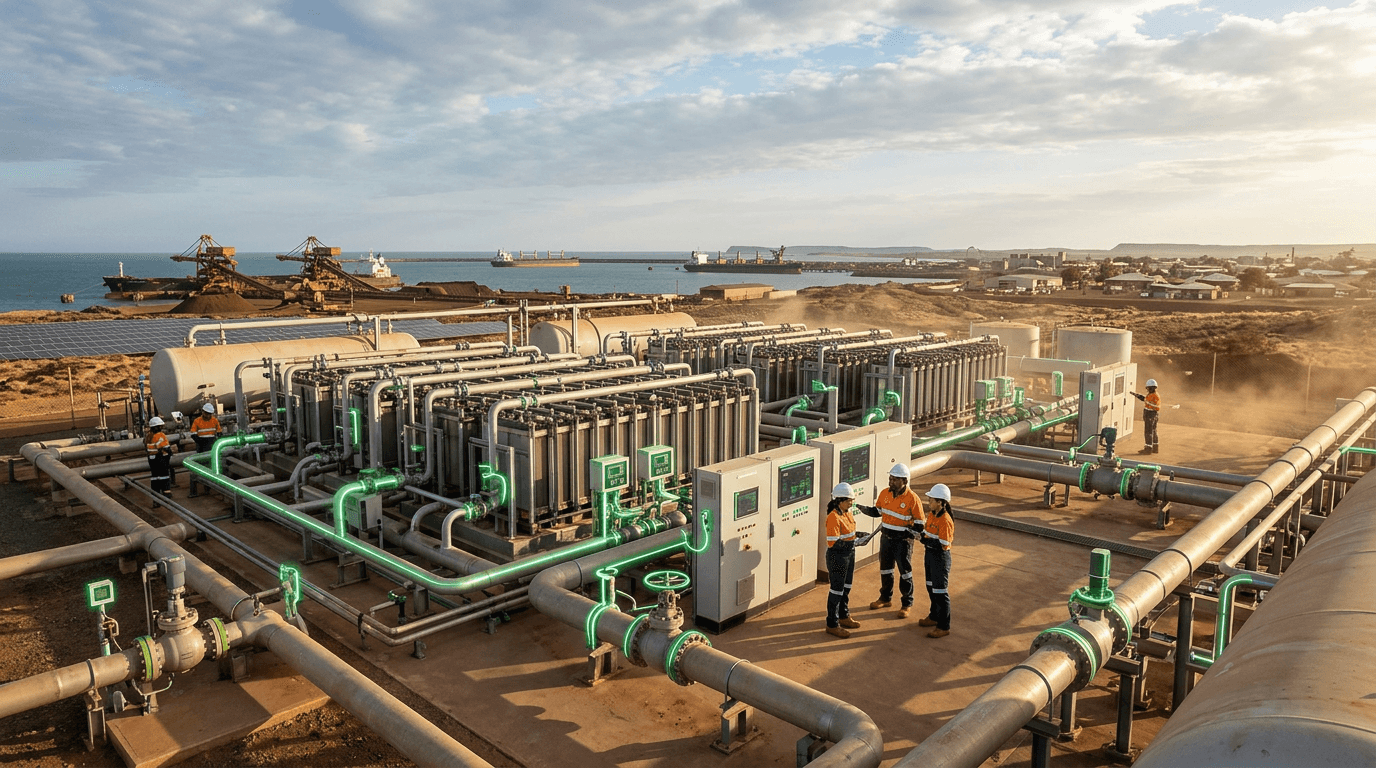

Australia is positioning itself as a future green hydrogen superpower, leveraging its vast renewable energy resources (solar irradiation among the world's highest, enormous wind potential) and proximity to Asian demand centers. The government has committed over A$3B through the National Reconstruction Fund, A$500M through the Regional Hydrogen Hubs Program, and production tax incentives introduced in February 2025. A flagship 6GW plant in Western Australia plans to begin construction in 2027 for green ammonia export.

Green hydrogen — produced by splitting water with renewable electricity — is the leading candidate to decarbonize industries that electricity alone cannot reach: steelmaking, shipping fuel, chemical feedstocks, and long-duration energy storage. Australia's competitive advantage lies in the combination of cheap renewable electricity, existing port infrastructure built for LNG and iron ore exports, and established trade relationships with Japan, South Korea, and Germany — all major hydrogen importers.

However, momentum has slowed. As of early 2025, most large-scale projects remained in pre-FID stages, with cost competitiveness versus grey hydrogen still a challenge. The Guardian reported in March 2025 that green hydrogen had "stalled in nearly every corner of Australia." The technology's strategic importance — as both an energy export and an enabler of green iron and green alumina processing — keeps government support flowing, but commercial viability at scale remains unproven. Success would reshape Australia's export identity from fossil fuels to renewable energy carriers.

Research this in Signals

Signals turns a topic into a sourced research record you can inspect and rerun. Your first scan is free, and this one starts with Export-Scale Green Hydrogen Production already loaded, so edit it or scan as is.