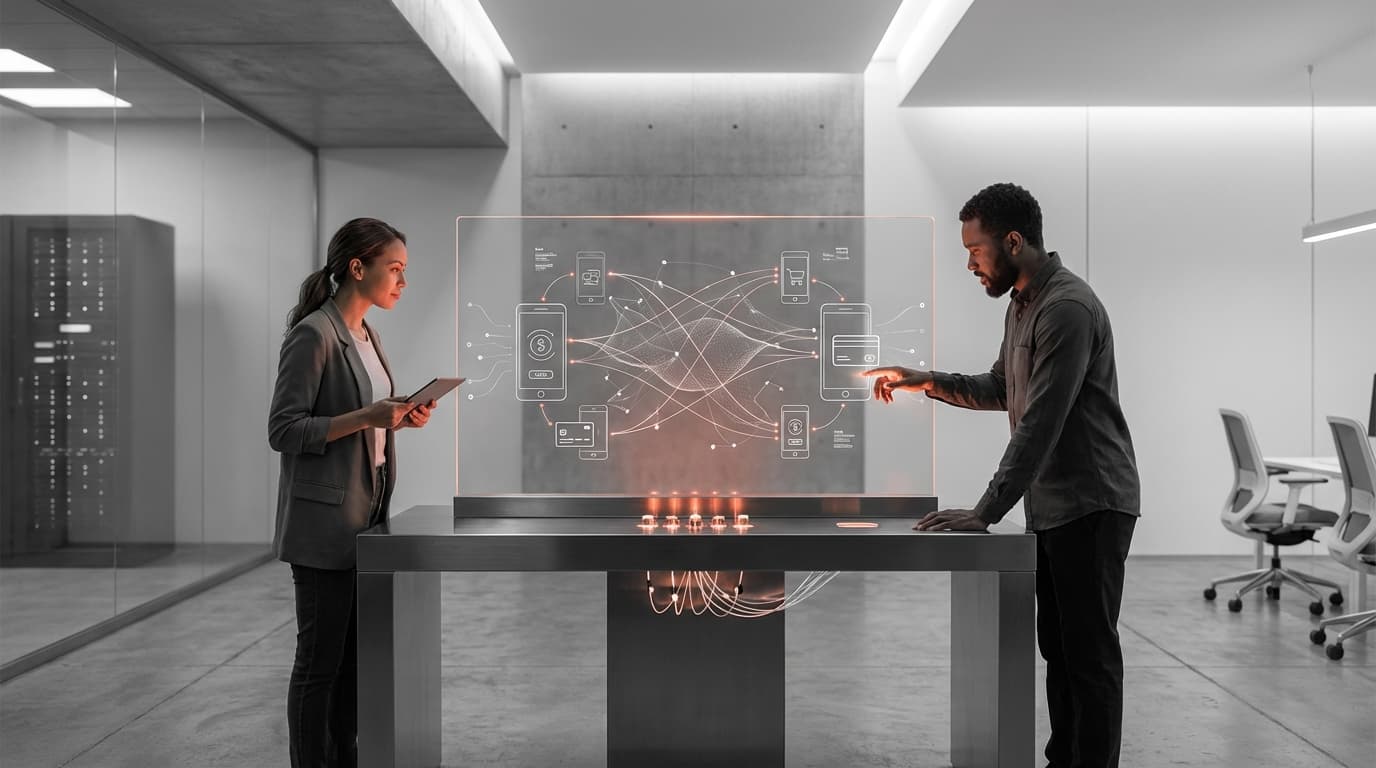

Fintech Alternative Credit Scoring

Traditional credit scoring systems have long relied on formal banking histories, credit card usage, and loan repayment records to assess an individual's creditworthiness. However, this approach systematically excludes billions of people worldwide who lack access to conventional banking services, creating a significant barrier to financial inclusion. In emerging markets and underserved communities, vast populations remain "credit invisible" despite demonstrating financial responsibility through their daily transactions. Fintech alternative credit scoring addresses this fundamental gap by leveraging non-traditional data sources to evaluate creditworthiness. The technology analyses patterns from mobile money transfers, utility bill payments, e-commerce purchase histories, and even social media behavior to construct comprehensive financial profiles. Machine learning algorithms process these diverse data streams to identify reliable indicators of repayment capacity and financial stability, creating credit scores for individuals who would otherwise be deemed unscoreable by traditional methods.

The business implications of alternative credit scoring extend far beyond simple risk assessment. Financial institutions face the dual challenge of expanding their customer base while maintaining acceptable default rates, and traditional underwriting methods often prove too conservative or simply inapplicable in markets where formal credit histories are scarce. By incorporating alternative data, lenders can make more nuanced risk assessments that capture the true financial behavior of potential borrowers. This capability enables banks, microfinance institutions, and digital lenders to profitably serve previously excluded market segments, transforming financial inclusion from a charitable goal into a viable business strategy. The approach also addresses operational efficiency challenges, as automated scoring systems can process applications at scale and speed impossible with manual underwriting, reducing costs while improving consistency in decision-making.

Alternative credit scoring has moved well beyond pilot programs to become a cornerstone of financial services in many developing economies. Digital lenders in markets across Africa, Southeast Asia, and Latin America routinely use mobile transaction data and e-commerce patterns to extend small loans to first-time borrowers, with some platforms processing thousands of applications daily. Research suggests that these alternative approaches can achieve default rates comparable to traditional scoring methods while dramatically expanding access to credit. The technology continues to evolve as new data sources emerge and machine learning techniques become more sophisticated, with some platforms now incorporating rental payment histories, educational credentials, and employment verification data. As regulatory frameworks adapt to accommodate these innovations, alternative credit scoring is increasingly recognized as an essential tool for achieving broader financial inclusion goals while demonstrating that advanced analytics can simultaneously serve social objectives and generate sustainable business returns.

Related Organizations

Develops bank-grade digital scorecards based on anonymous smartphone metadata.

Mobile technology and data science company providing loans to the underserved in emerging markets.

AI fintech company providing credit insights based on telco data.

Personal finance app providing loans using machine learning on mobile data.

Personal financial management platform in LATAM using utility payment data for scoring.

LenddoEFL

Singapore · Company

Combines psychometric testing and digital footprint analysis for credit scoring.

Provides AI software for credit underwriting that includes automated explainability for compliance (Zest Automated Machine Learning).

Provides 'first-party data' credit scoring via interactive virtual interviews.

Cross-border credit bureau enabling immigrants to use foreign credit history.

Upstart

United States · Company

AI lending platform that partners with banks to price credit using non-traditional variables.